how to write a budget

simple finances, part three

Welcome to mamaeats, a twice-weekly newsletter (Tues. & Sat.) inspired by a simple + seasonal home life. I’m a mother of three, avid reader, gardener, and home cook who focuses on nourishing, plant based, whole food meals. Subscribe below for weekly meal plans, reading and garden talk, and simple living inspiration.

Hello! Today’s newsletter is all about writing a budget. It is #3 in my personal finance series, the other two are called: simple finances (an overview of the basics of simple personal finance) and my payday routine for consistent saving (my routine I do each and every time I get paid to ensure our financial health). I recommend reading them all to get the most benefit, especially if you’re just starting out..

Whether you make little money or lots of money or somewhere in between, a budget is a non-negotiable. It makes your money work for you, not the other way around. Essentially, a budget means you have a plan— you decide in advance how you will spend the money you make, which maximizes its value as each dollar has a plan and works for you. It means that you keep both long and short term goals in sight, avoid impulse purchases, and make progress towards those goals.

I can’t tell you how much peace of mind this brings. It’s what has enabled us to save a relatively large portion of our income and not incur debt even though we didn’t save early in life, and our income throughout has been either low or modest.

Below, I’m outlining my personal way, but keep in mind there are many ways to budget! If this way doesn’t resonate, try another way, but don’t throw the baby out with the bathwater and give up altogether.

set a date

Set aside a date each month on which you will write the budget for the upcoming month. I do this the last Sunday of the month. It’s essential to set it like an appointment, otherwise it’s very likely that life will get in the way and you won’t get it done!

* It’s also helpful to set a date each week where you do a 10-15 minute check-in to look at balances and transactions in your accounts to make sure you’re not going over budget. For me, it’s Friday mornings.

If you are budgeting alongside a partner, include them in the meetings! Bribe them with cake if you need to. Both parties must be aware of the finances, at least the broad strokes.

Decide what method you’ll use to write/track the budget. You’ll need somewhere you can track day to day spending, check off when bills are paid, and to write the budget in.

I prefer writing and tracking the budget on paper (a good old $2 graph paper notebook; writing things down physically means I stay on track better as it’s more tangible), but I also use Empower’s free personal finance managing tool, which has a budget feature that automatically tracks spending across categories, to get a clear overall financial picture, and to double check spending through the month.

There’s lots of other analog and digital methods, too: ledger books, specific budget notebooks, Excel spreadsheets, apps (such as YNAB and Every Dollar), and online accounts like Empower. Chime in in the comments if you have a particular favorite method!

add up the income

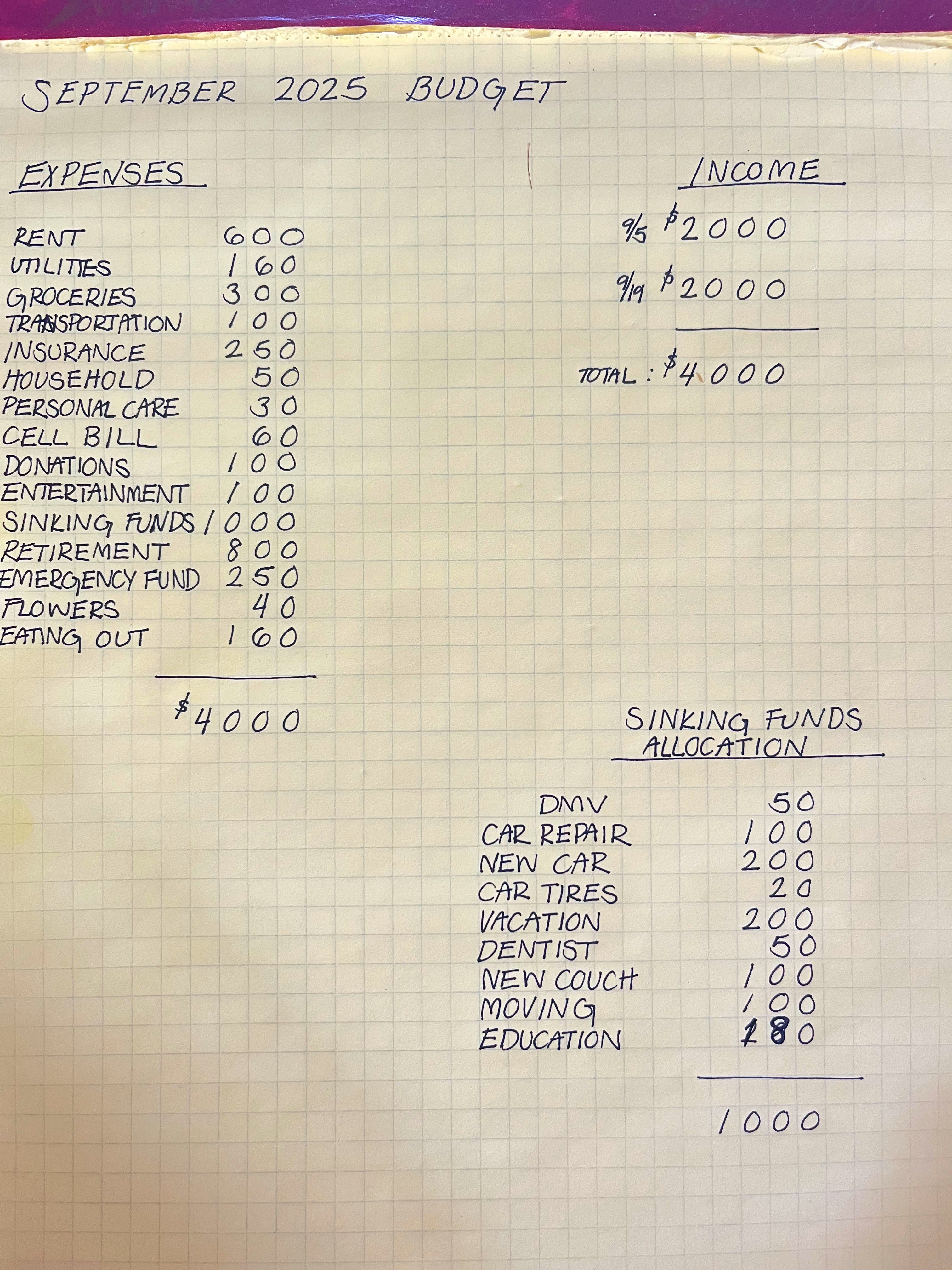

Determine how much money will be coming in this month (income). List every paycheck you will make along with its date, and add it up, along with any other sources of income you may have. This is what you have to work with.

add up the hard expenses

Determine your hard expenses. This will be your bare bones budget, ie your essential living expenses: rent/mortgage, utilities (estimate based on last year’s same month’s bill), groceries (go through bank statements and make a good guestimate based on what you have historically spent per month and what you feel is reasonable), transportation, loan installments, insurance, childcare etc— anything that MUST be paid so you can get to work, feed the household, have shelter, electricity, etc. Add these expenses up.

determine your savings

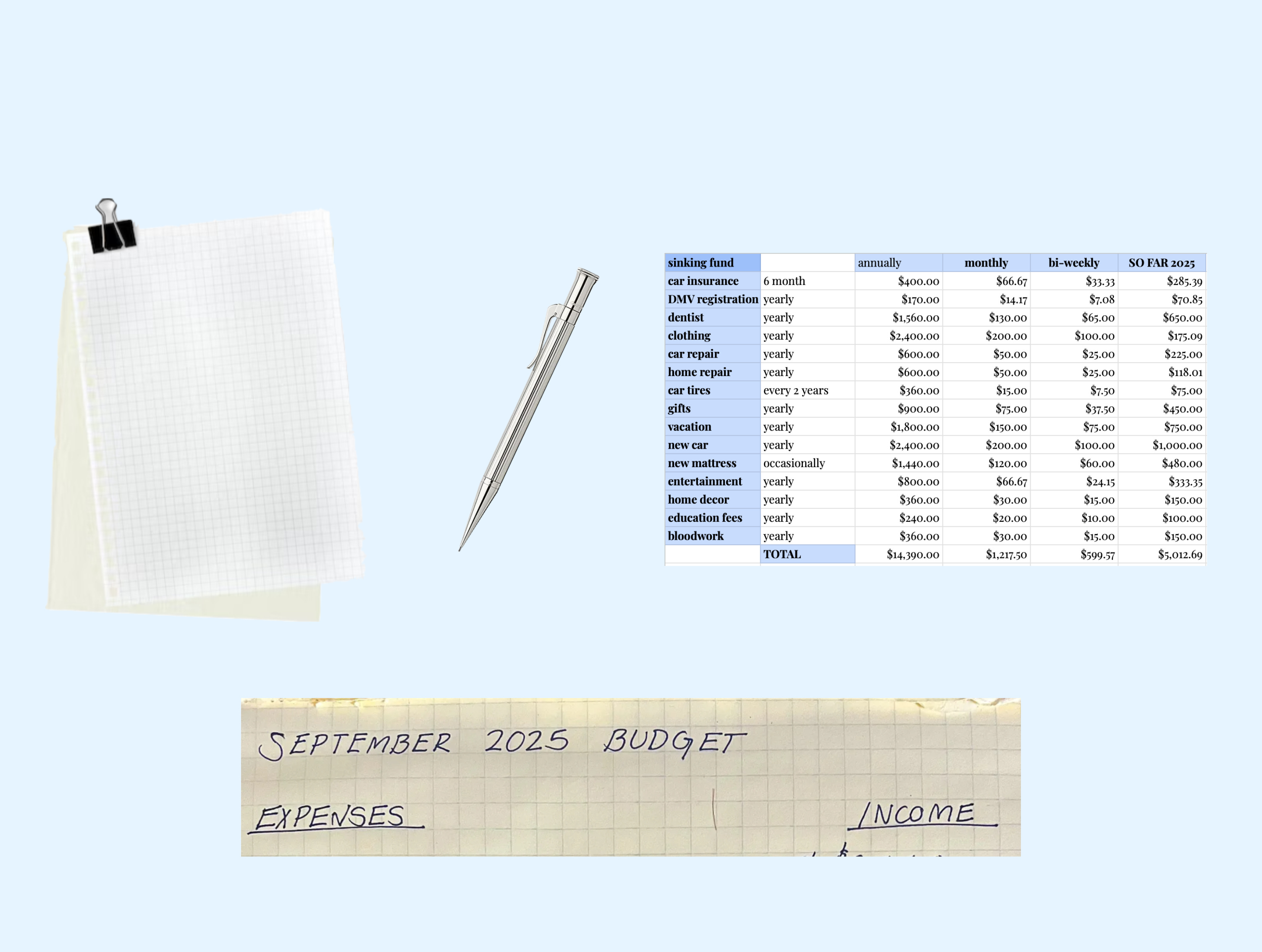

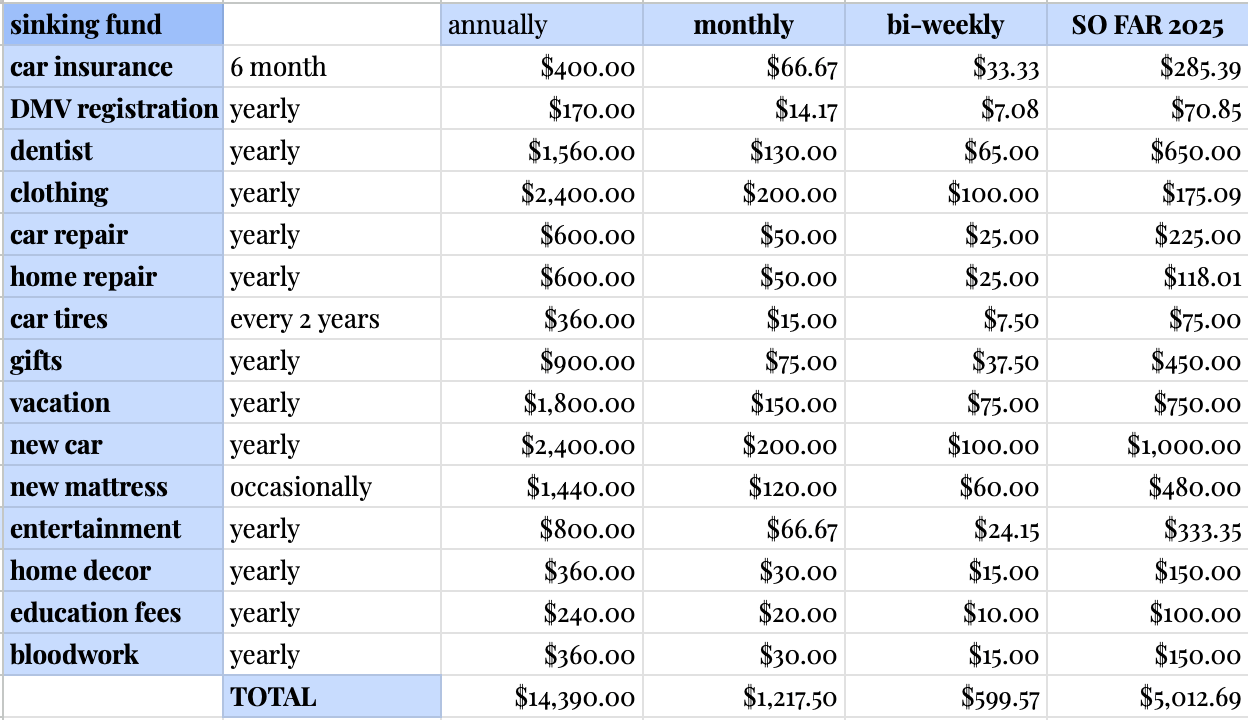

Decide how many savings pots you will have and for what. For us, this is sinking funds (see more detailed notes here1) and retirement accounts. Decide how much you will save; you may prefer to set a number or a percentage or both. I save a percentage (20% is a good rule of thumb, but will depend on circumstances and goals) of our take home pay for retirement, and then a specific number for sinking funds.

calculate and allocate leftovers for soft expenses

I consider soft expenses “wants” — everything outside of actual needs (the hard expenses listed above). Subscription accounts (Spotify, Netflix, memberships), eating out, takeaway coffees, recreation expenses, alcohol, beauty treatments, whatever it may be for you.

There is space for these creature comfort expenses, but only if you have the income for covering step 3 and 4: your hard expenses and your monthly savings, which take priority. You will probably have to sacrifice things you want to attain your financial goals. Financial health is so worth it for peace of mind.

Subtract your savings amount and hard expenses from your income, and what is leftover is what you have to spend on soft expenses. List out the soft expenses you will have, and allocate amounts to them, starting with the highest priority ones, until you get to a zero balance.

adjust as needed

Perhaps you made more money than expected, or your utilities bill came through and was higher than you budgeted for. You’ll have to adjust. Allocate the extra money to either spend on a soft expense, add to a savings account or a sinking fund. Find the extra money by cutting a soft expense.

Budgeting never is exactly perfect because life isn’t, but over time you’ll become better at noticing things, preparing for them, and getting a good idea of how your expenses flex. It’s no big deal if things go awry- just fix it as best you can and start over next month!

the very first time

The first time you write a budget, or when you have a new situation (perhaps your life circumstances have changed, your age, you start budgeting together with a partner, or just simply start a new year), you''ll need to go through a thinking process. Here are a few to get you started.

What are my financial goals for the year ahead? What are my financial goals over the next 5 years, decade, or beyond? Perhaps you’d like to save more money towards retirement, or have a specific spending goal (new car, house, vacation…), want to regularly donate money to a cause, or pay off your debt. A clear goal will motivate you and make it easier to follow the budget. With your goals, it’s good to be ambitious while also being realistic.

What am I saving for? How much do I need to save? How long do I have to save for it? Be sure to plan for non-monthly expenses here, which I like to allocate to sinking funds (see footnotes)

If I’m not able to save as much as I’d like, what is my long term plan to get there? Find another job that makes more money or has better benefits? Have a side job? Cut soft expenses? Look for another home that entails more modest expenses for renting/owning?

What are you willing to compromise on money wise? What are you not? Get clear on your priorities for spending.

The very first time, it will also be very helpful to look back on a year of transactions/bank statements/utility statements to get an idea of averages of monthly expenses, annual/non-monthly expenses, and other things you’ll most likely forget to plan for. The first year you budget, you’ll find yourself needing to adjust amounts, add and take away categories quite often, I think.

If you have a very hard time overspending on categories or find things overwhelming, it can help to simply pull out cash for the areas you overspend, as it’s impossible to go over when you have a tangible amount to work with. Some people exclusively use this envelope system for say, groceries, to avoid impulse spending.

Lastly, have fun with it, try not to get frustrated, and just stay as consistent as you can. You’ve got this.

I hope this newsletter (and the others in this series) has been helpful for you. Please do ask questions in the comments if there’s something you need help with. I’m absolutely not any kind of an expert, but I am passionate about personal finance!

Thank you for giving me the privilege of your time by being here and reading my little newsletter. I truly love being here and writing for you, but it does take significant time and effort. If you enjoyed this, please consider becoming a paid subscriber if you are not already, and have the means. Doing so gives you access to all the archives and recipes (find the recipe index here), as well as cook-along videos which go with most recipes, periodic video diaries, reading lists, and more. If you can’t swing a paid subscription right now, I’m always delighted to receive a one-off tip via my ko-fi—thank you! I appreciate you all so much.

See you Saturday, with the meal plan for the week ahead. xx A

Sinking funds are non-monthly expenses that you know will come up each year, or perhaps you don’t know when they’ll come up, but you know they will need to be paid for at some point. These are so important to plan for, as they can really throw off a monthly budget. You’re basically taking an occasional expense and paying for it each month/pay period.

For example, perhaps you know your refrigerator or car or computer is on its last legs and is going to need to be replaced soon. Price out what the replacement cost will be and draft an amount per month or per paycheck that will be need to set aside to reach those goals. Or, your car insurance is billed annually, or you’ll need to pay your kids school fees, or for Christmas gifts. Determine what you’ll need to spend, then divide by 12 for each month or by how many paychecks you’ll have in a year to get the amount to set aside to have it fully paid for by the time it’s due.

Here are our current sinking funds, to get an idea:

car insurance; annually

DMV insurance; annually

dentist; for what our insurance doesn’t cover

clothing; I have a set budget for the year

car repairs; oil changes, other repairs, parts, and maintenance

bike repairs; flat tires, new parts, labor, new bikes

home repairs; for things like replacing worn out sheets, towels, faucets, dishes, furniture etc, parts to fix appliances, repairs, renting a carpet cleaning machine

car tires

gifts; includes all gifts and any extras, such as party expenses, wrapping paper etc

vacation; annual summer vacation, camping trips, supplies needed for these things, such as new suitcases, parking fees, airplane tickets, extra gas, eating out…

new car; for when the old one gives out or is more expensive to repair than it’s worth. We always buy used and pay cash.

firewood; our yearly firewood purchase

kids sports; uniforms, fees, ccoach gifts, gear, parking or entrance fees

garden; for once yearly or bigger occasional expenses such as bare root roses, tulip bulbs, tools

I keep most of our sinking funds in a high interest savings account (I like Marcus by Goldman Sachs, I have used them for a while and find they have a very simple and clear web interface, competitive rate, quick transferring, and good customer service. Here is a referral code if you’d like to try them, it gives you an. extra .25% in interest over 3 months.) I keep a few in our regular bank savings account (clothing and gifts, things that get dipped into regularly) for ease.

You can read more about sinking funds here.

i always try to write down my expenses, savings etc ..... but always struggle and be consistent. thank you for sharing all these tipps. ❤️

Amanda, This was so grounding to read — especially the reminder to look back at a full year of transactions. I always underestimate how much that matters.

I’ve found it really helpful to convert my bank statements into spreadsheets so I can actually see my patterns. I use DataRiver.co for that, and it’s made budgeting feel much less intimidating. Thank you for sharing this so generously 💛